Assess Your Financial Readiness for Buying a Property 2026

Each section includes practical tips, sub-points, and action items so you have a clear, step-by-step roadmap to ensure you’re financially prepared for homeownership. We also have a dedicated Task Page to help you stay organized every step of the way!

Assess Your Financial Readiness

Determine Your Budget

Income and Savings Analysis

– Monthly Cash Flow: Calculate your net monthly income and subtract recurring expenses (rent, utilities, groceries, insurance) to see how much is left for a mortgage.

– Emergency Fund: Even after a down payment, you should keep some savings for unexpected expenses (car repairs, medical bills) to avoid missing mortgage payments.

– Future Financial Goals: Consider other upcoming costs (like starting a family, going back to school, or starting a business) that might affect how much you can comfortably commit to housing.

Mortgage Impact on Monthly Cash Flow

– Principal and Interest: Estimate what your monthly mortgage payment would be based on current interest rates.

– Property Taxes: Research average tax rates in the area where you plan to buy. Taxes can significantly affect your monthly escrow payment.

– Homeowners Insurance and PMI: Factor in insurance costs. If your down payment is below 20%, private mortgage insurance (PMI) may also apply.

Pro Tips: Understanding how much you can comfortably spend on a mortgage ensures you don’t overextend your finances and set yourself up for success.

Review Your Credit Score

Why Credit Matters

– Interest Rate Impact: A higher credit score can translate into lower interest rates, saving you thousands over the life of the loan.

– Loan Qualification: Lenders have minimum score requirements. A poor score could mean larger down payments or higher interest rates.

Steps to Improve Your Score

– Pay Down Debt: Credit cards, personal loans, and car loans all factor into your debt-to-income ratio. Reducing these helps your credit utilization.

– Check for Errors: Dispute inaccuracies on your credit report (e.g., incorrect late payments, closed accounts still showing open) through the credit bureaus.

– Avoid New Lines of Credit: Right before applying for a mortgage, steer clear of opening new credit cards or taking out car loans if possible.

Pro Tips: A strong credit score helps you secure better loan terms, which saves you money on your mortgage and increases your borrowing capacity.

Save for Down Payment & Closing Costs

Down Payment Requirements

– Traditional/Conventional Loans: 10–20% down is common, but some lenders permit as low as 3–5% if you meet certain criteria.

– FHA Loans (U.S.): Typically as low as 3.5% down if you meet credit score requirements.

– Other Programs: VA loans for military veterans, USDA loans for rural areas, or local grant programs may offer 0% or low down payment options.

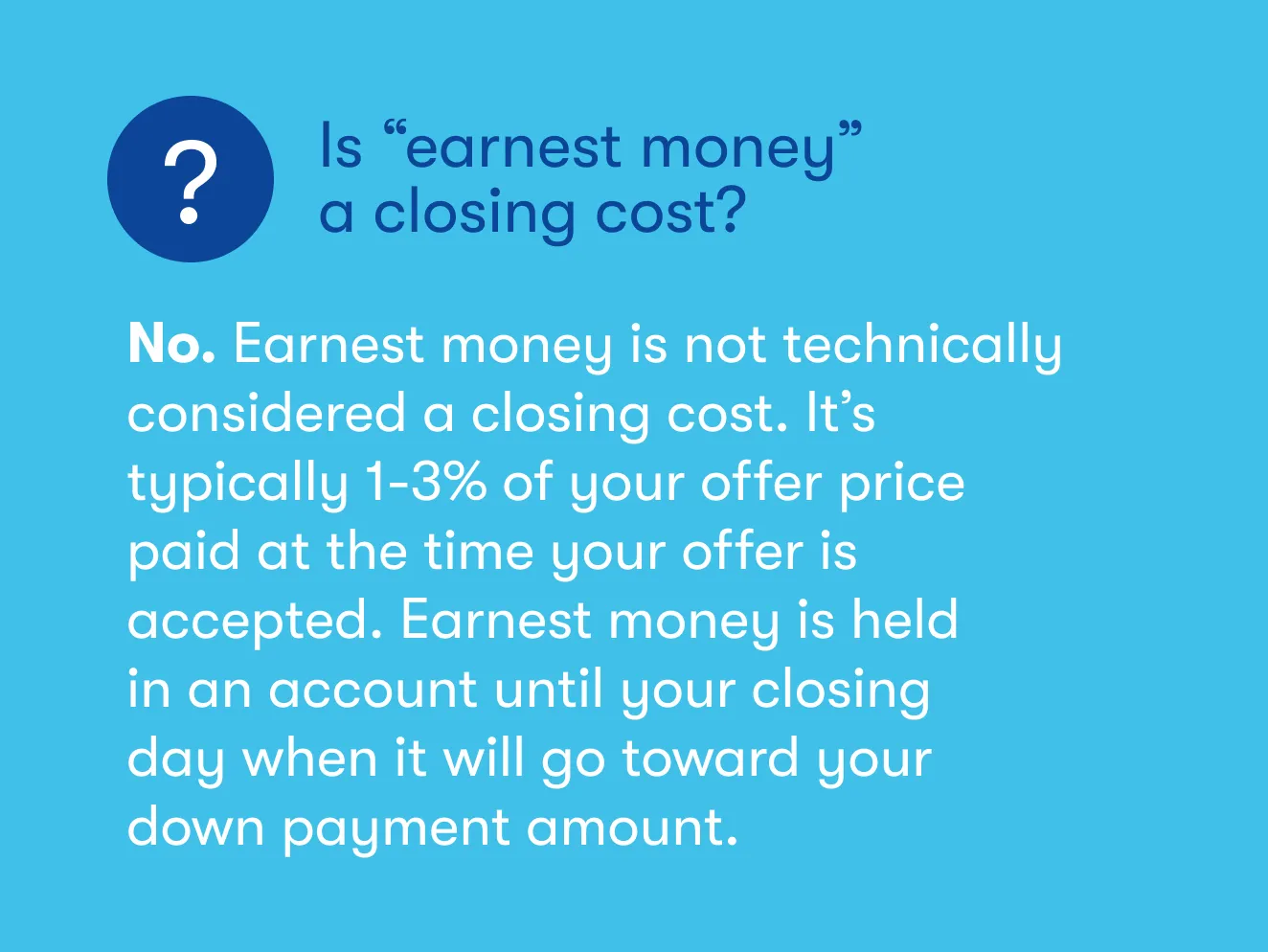

Closing Costs

– Range of 2–5%: Includes fees for appraisals, inspections, title insurance, taxes, and lender origination fees.

– Seller Concessions: In some markets, sellers might cover part of the closing costs to sweeten the deal but this isn’t guaranteed.

Pro Tips: Saving enough for the down payment and closing costs ensures you’re fully prepared to move forward with your property purchase.

Action Items

– Use a Mortgage Affordability Calculator: Experiment with different scenarios for interest rates, loan terms, and down payments.

– Create a Savings Plan: Automate savings or consider part-time work to increase savings for your down payment.

– Monitor and Improve Your Credit Score: Regularly check your credit report and address any issues to improve your credit score.

Pro Tips: Completing the action items ensures you’re financially prepared to make an offer and manage your future mortgage payments.

Conclusion

Assessing your financial readiness is the first step to homeownership. By defining your budget, reviewing your credit score, and saving for both down payment and closing costs, you’ll set yourself up for a smoother buying process. The more work you do upfront, the fewer surprises you’ll encounter down the line.

Some Tools To Use For You To Assess Your Financial Readiness For Buying A Property

Organizing the process and staying on top of every phase of buying strategy will save you both time and money. Stay diligent and use the tools provided to keep your purchase moving forward with confidence!

Credit Scores Companies

Explore reliable credit score companies both in the USA and Canada and understand how strong your credit or where you need to improve!

How To Save For A House (Plus EVERYTHING else you will need to know)

Lets get back to the basics in terms of saving enough for a down payment to buy real estate, what you’ll need for lenders to give you money, and some things to prepare for before you start buying a house.

UNDERSTAND how Credit Scores work | Guide for Canadians

If you want to borrow money from the bank, for an investment loan, margin account, or to buy a house, you need to have a good credit rating. This video is the ultimate guide to how credit scores work in Canada.

How Much Home You Can ACTUALLY Afford in 2024 (By Salary)

Really do your due diligence when thinking about buying a home!

Knowledge Quiz: Assess Your Financial Readiness for Buying a Property

Open Quiz

5 quick questions - see how much you learned!

1) When determining your budget, which step correctly estimates how much you can put toward a mortgage each month?

Answer: B

The page’s “Income and Savings Analysis” says to use net monthly income minus recurring expenses to see what’s left for a mortgage.

2) If your down payment is less than 20% on a conventional loan, which additional monthly cost may you owe?

Answer: B

The “Homeowners Insurance and PMI” bullet notes that PMI may apply when the down payment is below 20%.

3) Why should you keep an emergency fund even after putting money toward your down payment?

Answer: C

The “Emergency Fund” bullet explains you should retain savings for surprises (repairs, medical, etc.) so your mortgage stays on track.

4) What closing cost range should a buyer generally budget for, according to the page?

Answer: B

The “Closing Costs” section lists a typical range of 2–5% (appraisal, inspection, title insurance, taxes, origination fees, etc.).

5) Right before applying for a mortgage, which action should you avoid to protect your credit?

Answer: C

The “Avoid New Lines of Credit” step says to steer clear of opening new credit right before you apply, to protect your score and terms.

More Investing Tips and Strategies Real Estate

Stay informed with the latest trends, insights, and updates in the real estate world.